The North American life and annuity market is not in a quiet period. Annuity sales reached $464.1billion in 2025 - the fourth consecutive record year, with sales having nearly doubled over the past five years1. Aging demographics, rising demand for protected retirement income, and a wave of product innovation are all pushing in the same direction. The market is growing. The appetite is there. The distribution channels are expanding.

And yet the technology most carriers and distributors run on was not built for this moment. It was designed for a market that moved more slowly, offered simpler products, sold through fewer channels, and operated in a more predictable regulatory environment. The gap between where the market is going and what the systems supporting it can actually do is widening every year.

This article maps what a complete L&A technology stack needs to look like in 2026 - what each functional layer needs to do, why it matters, and why the pieces only work when they are genuinely connected rather than assembled from independently procured tools.

The Pressure on the Stack

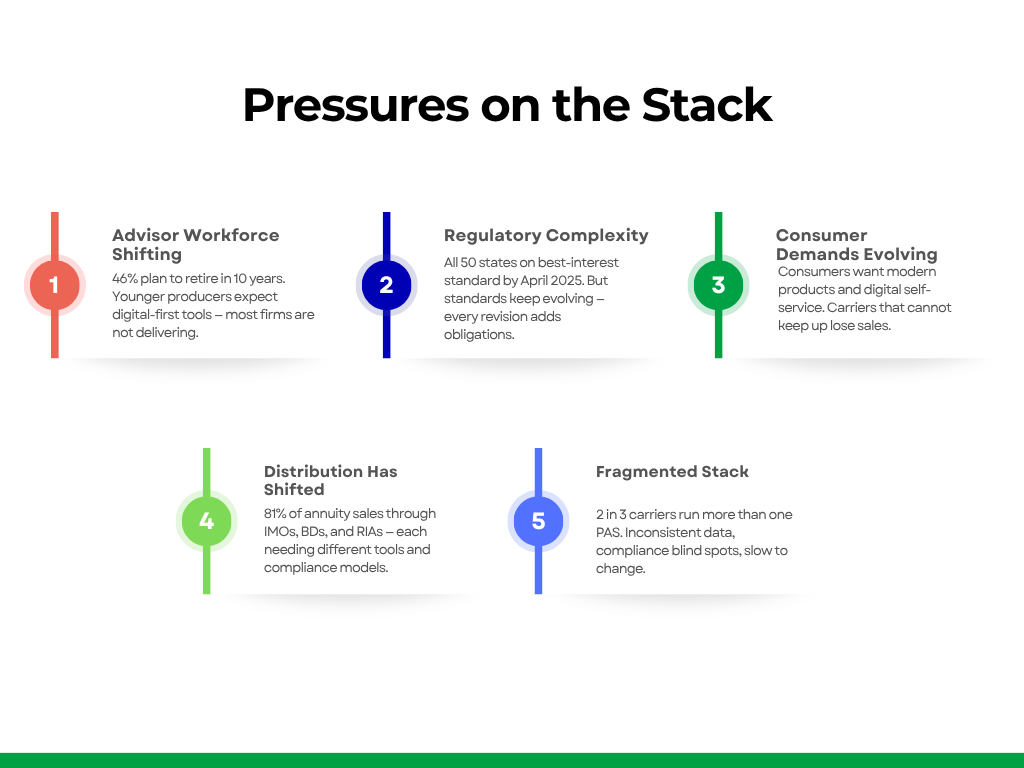

The L&A market is not struggling - it is under pressure from its own growth. Five structural forces are reshaping how carriers and distributors need to operate, and each one creates a specific demand on the technology stack that either exists or does not.

a) The advisor workforce is changing

46% of financial advisors plan to retire within the next ten years2. More than one in four are already 65 or older. The experienced producers who have built careers selling life and annuity products are leaving the industry at a faster rate than they are being replaced.

But the more immediate technology problem is not the retirement wave - it is what the incoming generation needs.

Younger advisors entering the market expect digital-first tools, faster onboarding, and compliance support built into the way they work rather than treated as a separate process. Most firms are not meeting that expectation. A carrier whose technology makes it hard for a new producer to get up to speed is not just losing efficiency - it is losing distribution.

The technology demand this creates is specific: advisor portals that reduce the time it takes a new producer to become effective, allow them to easily compare products, capture customer details digitally, show illustrations instantly, and make the sales process as intuitive as the tools advisors use in every other part of their professional lives.

b) Regulatory complexity that does not sit still

By April 2025, all 50 states had adopted a best-interest annuity sales standard aligned with NAIC Model Regulation 2753 - New Jersey became the final state to comply. On the surface this looks like the regulatory picture has settled. It has not.

Standards at both state and federal level keep moving independently of each other. Every revision changes what information must be collected from the consumer, what disclosures must be made, what documentation must exist, and what obligations extend to policies already in force - not just new sales. For carriers managing this manually, every regulatory update is an operational project: new training, new forms, new review steps, new audit requirements.

The technology demand is clear: compliance cannot sit outside the core business. It needs to be embedded in the workflow from the moment a recommendation is made, capturing what was considered, what was recommended, and what was disclosed - automatically and in real time.

c) Consumer demands are evolving faster than systems can keep up

What consumers expect from life and annuity products has changed significantly. They want products that grow with the market, protect against downside, and pay guaranteed income for life - and they want to manage those products digitally, on demand, without calling anyone. FIA, RILA, and hybrid product sales have grown dramatically over the past decade as carriers race to meet this demand. Every new product line requires the stack to configure it, illustrate it, apply for it, administer it, and service it. In most carrier environments today, launching a new product variant requires months of IT development - and the self-service experience consumers expect is rarely built into the platforms that administer those products.

Every new product line - a new crediting method, a new rider structure, a new benefit bundle - requires the technology stack to configure it, price it, illustrate it, apply for it, administer it, and service it across a policy lifetime that can span decades. In most carrier environments today, launching a new product variant requires months of IT development. By the time the product is ready ,the market window it was designed to capture may have moved.

The technology demand: a configurable product engine where business teams can define new products and rules without triggering a development cycle every time, and self-service capabilities that let consumers manage what they buy without needing to call anyone.

d) Distribution has moved to channels carriers do not control

Third-party distribution now represents 81% of annuity sales in the US4. IMOs, broker-dealers, and RIAs have become the primary route to market for most carriers. Each of these channels operates differently - different compliance obligations, different compensation structures, different advisor expectations, and different experiences they need to deliver to their own clients.

A carrier whose technology was built around a captive agent force cannot serve this reality. Equipping an IMO network requires different tools, different journeys, and different compliance models than equipping a broker-dealer or an RIA. Trying to serve all three through a single system designed for one is where distribution relationships quietly break down.

The technology demand: channel-specific experiences built on a common platform -the same underlying product and data, but a different journey, differentcompliance checks, and different compensation model depending on who is selling and through which channel.

e) The stack itself is fragmented

Two-thirds of life and annuity carriers run more than one policy administration system. Some run more than ten.5

This is not negligence - it is the accumulated result of decades of acquisitions, product line expansions, and point solutions deployed to solve specific problems at specific moments. Each one made sense at the time.

The consequence is a technology estate where data does not move cleanly between systems, changes to one system ripple unpredictably into others, compliance teams cannot get a single view of what happened in a transaction, and where IT teams spend more time maintaining integrations than building capability. The result is integration complexity, inconsistent data, and a technology estate that is slow and expensive to change.

The technology demand: a platform where the functional modules share a common data layer and workflow foundation - so that a change in one area does not require rework across the entire estate.

What the Stack Needs to Do

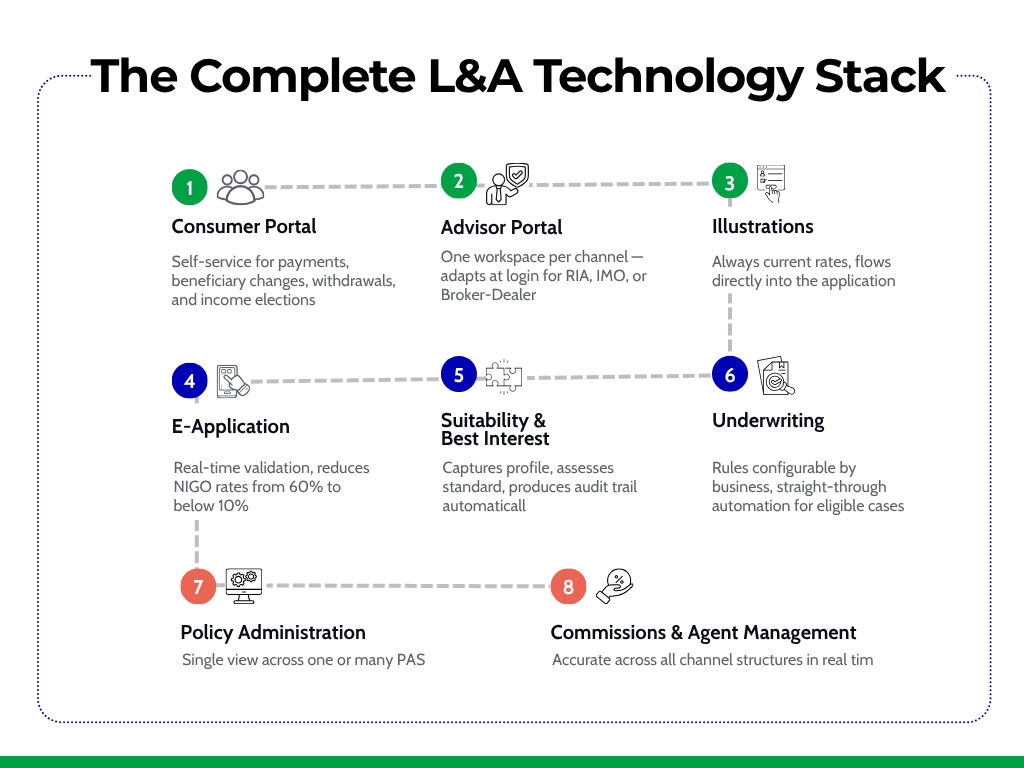

The five forces above do not just describe market conditions - they define specific technology requirements. A complete L&A stack needs to cover eight functional areas, each one the direct answer to at least one of the pressures above. None of these capabilities is new. What is new is the expectation that they are composable and work together as one platform rather than as a collection of separately procured tools.

1. Consumer portal

A modern consumer portal covers the full in-force lifecycle - not just basic account access. Consumers can make payments, update beneficiaries, request withdrawals, elect income options, and grant access to family members or advisors, all without picking up the phone.

A well-designed portal goes further - surfacing relevant information at the right moment, guiding consumers through complex transactions, and keeping the carrier relationship active across decades of policy ownership rather than dormant between point of sale and claim. Without this capability every routine interaction becomes a manual servicing event, consuming operational cost that compounds across millions of in-force policies.

2. Advisor portal

Advisors are the primary sales channel for life and annuity products. The technology they use every day influences how much they sell, how efficiently they sell it, and which carriers they choose to sell for. A fragmented experience - separate tools for proposals, e-applications, case tracking, and commission visibility - creates friction at every step and costs distribution quietly over time.

A modern advisor portal is a single workspace that adapts at login depending on whether the user is an RIA, an IMO, or a Broker-Dealer. The same underlying platform serves all three, but each sees the experience and the workflows relevant to how they operate. For a new producer joining a carrier, this is often the first interaction they have with that carrier's technology - and it directly shapes whether they stay and sell.

3. E-application

The electronic application is where a sale either moves forward or stalls. 60% of paper-based L&A applications are submitted NIGO (not-in-good-order)6. Every NIGO is a delayed policy issuance, a frustrated advisor, and a gap in the compliance documentation that should have been captured at point of sale. Chasing missing information after submission is expensive, slow, and avoidable.

A configurable digital application validates in real time - catching missing information, checking advisor licenses and appointments, confirming that compliance requirements have been met before the application reaches the carrier's new business team. When this works properly, digital platforms bring NIGO rates below 10%. The difference between 60% and 10% is the difference between an advisor who keeps submitting business and one who quietly moves to a carrier whose process works better.

4. Suitability and best interest

With all 50 states now on a best-interest standard, suitability is no longer a checkbox at the end of a sale. It is a continuous obligation that begins when a recommendation is made and extends through the in-force life of the policy - in New York, Regulation 187 applies the same documentation requirements to changes made to existing policies as it does to new sales.

Managing this manually creates inconsistency across distribution channels, delays in the sales process, and audit exposure when documentation is incomplete or assembled after the fact. Suitability needs to be embedded in the sales workflow - capturing the consumer's financial profile, assessing whether the recommendation meets the applicable standard in the relevant jurisdiction, documenting the rationale, and producing an audit trail that can withstand regulatory scrutiny. All of this within the workflow, not alongside it.

5. Illustrations

Before an annuity is sold, it is shown. Illustrations are the primary tool through which advisors explain how a product works, what it is projected to pay, and how it compares to alternatives. When illustration tools are disconnected from the product engine, the rates shown may not reflect what the carrier is currently offering, the assumptions may have drifted from current product terms, and the output cannot flow directly into the application - creating inconsistency between what the consumer was shown and what was applied for.

An integrated illustration capability is always connected to the product engine, always reflects current rates and product features, and produces output that flows directly into the application process. When a product changes, the illustration changes with it - not weeks later after a manual refresh.

6. Underwriting

Once an application is submitted, it needs to be assessed - eligibility confirmed, risk evaluated, and the policy either issued, referred for further review, or declined. In most carrier environments today, underwriting rules sit in systems that cannot be updated without IT involvement. A regulatory change or a new product rule requires a development cycle before it can be enforced, creating a lag between what the business needs and what the system can do.

A modern underwriting capability puts rules configuration in the hands of the business - not the IT queue. Straight-through decisions are automated for cases that meet the criteria. Exceptions are routed for human review with full context already assembled. Nothing between the e-application and policyissuance should require data to be re-keyed or handed off manually.

7. Policy administration

The policy administration system is the system of record for everything that happens after a policy is issued - billing, value calculations, transactions, and servicing across a lifetime that can span decades. Two thirds of carriers run more than one PAS (Policy Administration System). The cumulative cost of that fragmentation - integration overhead, inconsistent data across systems, slow product launches that require touching multiple systems simultaneously - compounds silently every year and makes the business progressively harder to change.

What carriers need is not necessarily a single replacement PAS. It is a layer that orchestrates across one or several policy administration systems so the business always has a single view of every policy regardless of which system holds it - and can launch new products, respond to regulatory changes, and serve policyholders without navigating the complexity of a fragmented estate every time.

8. Commissions and agent management

Commission errors damage distribution relationships faster than almost anything else a carrier can do wrong. In life and annuities the calculation complexity is genuine - multi-level hierarchies, split commissions, chargebacks, grid-based compensation, and entirely different structures for IMOs, broker-dealers, and RIAs all running simultaneously across the same carrier.

A commissions platform that calculates accurately across all structures, provides agents and distributors with real-time visibility on what they have earned, and integrates with the carrier's financial systems without manual reconciliation is not a nice-to-have. It is the operational foundation of a distribution relationship that lasts.

Why It Only Works as One Thing

Eight modules. Each one necessary. But a carrier that procures best-in-class solutions across all eight and connects them through point-to-point integrations, custom middleware, and manual handoffs still has a fragmented stack. Data still in silos. Changes still cascade unpredictably. Compliance teams still cannot get a complete picture of a transaction that touched four different systems. New product launches still require rework across the estate. The individual modules are better, but the fundamental problem has not been solved.

What makes the difference is a shared foundation - a common layer through which all transactions flow, against which all state is tracked, and from which a complete audit trail can always be produced. Without it the modules are neighbours. With it, they are a platform.

One approach to building this foundation is an Insurance Workflow Language - a portable, auditable, business-readable workflow definition that serves as a shared contract between business and technology. Compliance can read it and review it. Developers can version it and see exactly what changed between releases. The platform executes it consistently across every system it touches.

The practical implications are significant. When a regulation changes, the workflow definition changes - not code spread across five different systems. When a new product launches, the journey is configured in the definition and deployed rather than developed from scratch. When an auditor asks what happened in a transaction, the workflow definition is the answer - a complete, readable record of every step, every decision, and every output.

A carrier that gets this right does not just have better technology. They have infrastructure that can adapt as the market, the regulation, and the products keep changing - without a development project every time something moves.

Life Bridge is built around this idea - a composable, AI-native platform for life and annuity carriers that brings every layer of the stack together under a common workflow foundation.

Sources

1 https://www.limra.com/en/newsroom/news-releases/2025/limra-final-u.s.-retail-annuity-sales-set-new-sales-high-totaling-$464.1-billion-in-2025/

2 https://www.jdpower.com/business/press-releases/2026-us-life-annuity-distribution-partner-experience-study

3 https://insurancenewsnet.com/innarticle/suitability-standards-for-life-and-annuities-not-as-uniform-as-they-appear

4 https://www.mckinsey.com/industries/financial-services/our-insights/redefining-the-future-of-life-insurance-and-annuities-distribution

5 https://www.deloitte.com/us/en/insights/industry/financial-services/modernizing-l-and-a-systems.html

6 https://fidx.io/resources/top-5-ways-to-eliminate-nigos